Latest Quarterly Results

Quarterly Report For The Financial Period Ended 30 September 2025

Financials Archive![]() Note: Files are in Adobe (PDF) format.

Note: Files are in Adobe (PDF) format.

Please download the free Adobe Acrobat Reader to view these documents.

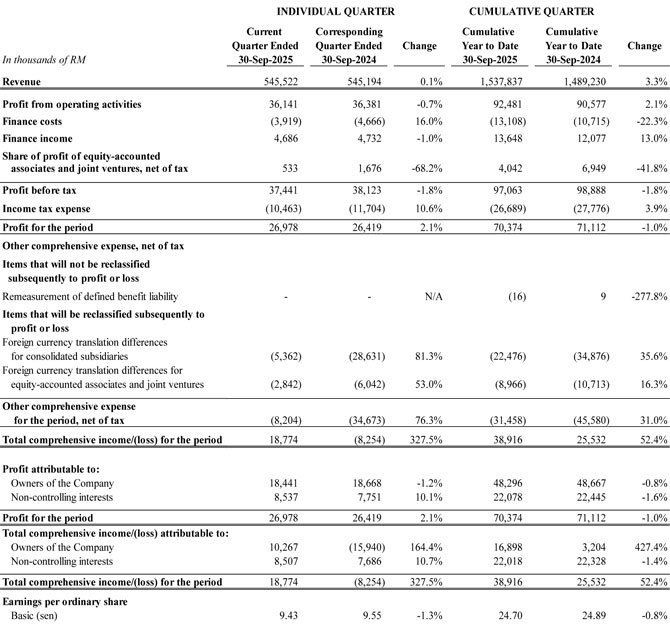

Condensed Consolidated Statements Of Profit Or Loss And Other Comprehensive Income

For The Quarter Ended 30 September 2025 - unaudited

The above condensed consolidated statement of profit or loss and other comprehensive income should be read in conjunction with the audited financial statements for the year ended 31 December 2024 and the accompanying explanatory notes attached to these interim financial statements

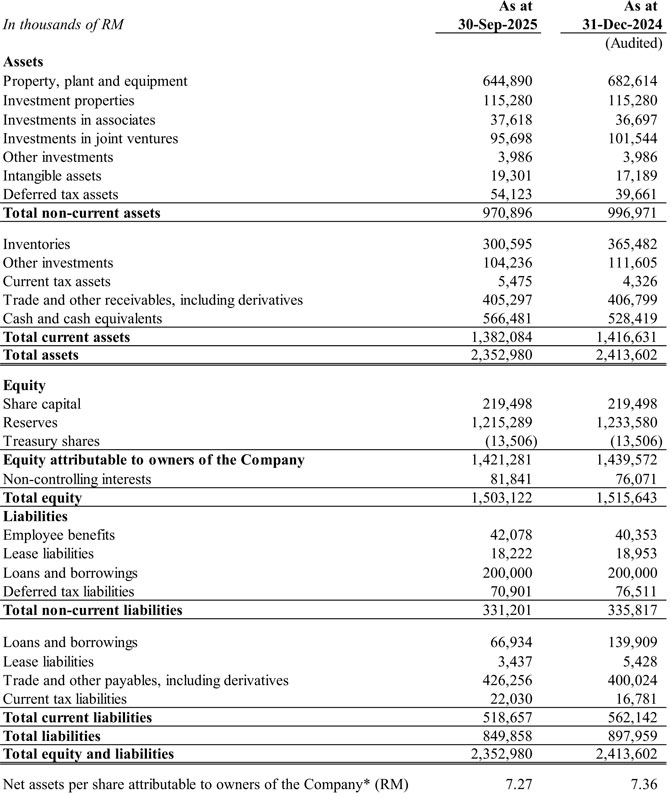

Condensed Consolidated Statements Of Financial Position

As At 30 September 2025 - unaudited

*Net assets per share is calculated based on total share capital in issue less treasury shares of 6,105,700.

The above condensed consolidated statement of financial position should be read in conjunction with the audited financial statements for the year ended 31 December 2024 and the accompanying explanatory notes attached to these interim financial statements.

Operating Segments Review

Statement of Financial Position

The Group's financial standing remained robust with shareholders' fund of RM1.5 billion and a net cash position of RM403.8 million as at 30 September 2025 (i.e. cash and cash equivalents plus other investments (current assets) and less bank borrowings). The Group's current ratio (i.e. Current Ratio = Current Assets/Current Liabilities) improved from 2.52 times to 2.66 times, primarily driven by better working capital management arising from faster inventory turnover and better payment terms to suppliers.

The Group's net assets per share decreased from RM7.36 as at 31 December 2024 to RM7.27 as at 30 September 2025. The decline was mainly attributable to the dividend payments totalling RM35.2 million to shareholders and RM20.0 million to non-controlling interests during the period under review. Additionally, the strengthening of the Malaysian Ringgit led to unfavourable foreign currency translation effects on the Group's foreign subsidiaries, associates, and joint ventures, further contributing to the reduction in net assets per share.

Statement of Cash Flow and Capital Expenditure

For the current quarter ended 30 September 2025, the Group recorded a net increase in cash and cash equivalents of RM38.1 million from RM528.4 million as of 31 December 2024 to RM566.5 million as of 30 September 2025. The positive cash flow movement was attributed to the following factors:-

- Net cash generated from operating activities of RM183.4 million that was mainly driven by pre-tax profit of RM97.1 million, coupled with lower inventory holding resulting in positive changes of RM60.8 million and higher trade and other payables balance resulting in positive changes of RM29.6 million;

- Net cash used in investing activities of RM14.0 million mainly for the purchase of tooling, machineries and equipment as well as the construction of a new production facility amounting to RM24.8 million, offset by the net redemption of unit trusts amounting to RM12.0 million; and

- Net cash used in financing activities of RM128.2 million mainly due to the payment of dividend to owners of the Company totalling RM35.2 million, payment of dividend to non-controlling interests totalling RM20.0 million, and net repayment of loans and borrowings amounting to RM73.0 million.

As of 30 September 2025, the Group's capital commitment stood at RM49.5 million comprising primarily the Group's investment in tooling, machineries/equipment and development costs for the supply of parts for new vehicle models and the construction of a new production facility. The capital commitment is funded internally and through bank borrowings.

The Group recognises that the retention of sufficient cash reserves is essential in the pursuit of growth and expansion. Thus, the Group's liquidity remains intact as the balance of IMTN of up to RM1.30 billion in nominal value, as of the date of this report, can be utilised for future capital investment, if and when required.

Analysis of Performance of All Operating Segments

Q3'2025 vs Q3'2024

For the current quarter ended 30 September 2025, the Group recorded revenue of RM545.5 million, a marginal increase of 0.1% compared to revenue of RM545.2 million in the corresponding quarter ended 30 September 2024. The revenue in Q3'2025 remained relatively flat, as the strong demand from certain OEM models was offset by the softening of export market.

Despite the higher revenue, the Group's profit before tax ("PBT") decline marginally from RM38.1 million in the corresponding quarter ended 30 September 2024 to RM37.4 million in the current quarter ended 30 September 2025 primarily due to unfavourable sales mix and margin compression arising from intense market competition. The lower share of profit from the Group's associates and joint ventures further impacted the Group's PBT.

Year-to-date 2025 ("YTD 2025") vs Year-to-date 2024 ("YTD 2024")

For the nine months ended 30 September 2025, the Group recorded higher revenue of RM1.54 billion, representing an increase of RM48.6 million or 3.3% compared to revenue of RM1.49 billion in the same period last year mainly due to full-period contributions following the commencement of supply for certain new OEM models since Q2'2024.

Despite the higher revenue, the Group's PBT declined marginally to RM97.1 million (YTD 2024: RM98.9 million) due to a slowdown in domestic OEM and export sales, affecting Suspension, Electrical & Heat Exchange, and Marketing divisions. The lower share of profit from the Group's associates and joint ventures, coupled with unfavourable sales mix and margin compression arising from intense market competition further impacted the Group's PBT.

Suspension Division

For the current quarter ended 30 September 2025, the Suspension Division recorded a 20.0% decrease in revenue (Q3'2025: RM47.8 million; Q3'2024: RM59.7 million) mainly due to weaker domestic and export sales. In line with the lower revenue and unfavourable sales mix, the Suspension division registered a LBT of RM1.5 million compared to PBT of RM0.1 million in the corresponding quarter last year.

For the nine months ended 30 September 2025, the Suspension Division recorded lower revenue of RM146.7 million (-17.7% compared to the same period last year ("YoY")) mainly due to the same factor mentioned above. In line with the lower revenue and unfavourable sales mix, the Suspension Division registered a LBT of RM2.7 million compared to PBT of RM3.8 million in the same period last year.

Interior & Plastics Division

For the current quarter ended 30 September 2025, the Interior & Plastics Division recorded a 3.4% increase in revenue to RM452.8 million (Q3'2024: RM437.8 million) mainly driven by the stronger demand for certain OEM models. Despite the higher revenue, PBT declined by 20.4% to RM40.5 million (Q3'2024: RM50.9 million) primarily due to unfavourable sales mix and margin compression arising from intense market competition.

For the nine months ended 30 September 2025, the Interior & Plastics Division recorded higher revenue of RM1.24 billion (+7.0%) against RM1.16 billion recorded in the same period last year mainly due to full-period contributions following the commencement of supply for certain new OEM models since Q2'2024. However, PBT declined by 10.1% to RM106.1 million (YTD 2024: RM118.0 million) due to the same reasons explained above. The higher PBT in same period last year was boosted by the upward price adjustment received from certain customers and the recovery of development expenditures for certain OEM models.

Electrical & Heat Exchange Division

For the current quarter ended 30 September 2025, the Electrical & Heat Exchange Division registered a 1.5% increase in revenue (Q3'2025: RM34.3 million; Q3'2024: RM33.8 million) mainly due to the commencement of supply for certain new OEM models since Q2'2025. In line with the higher revenue, the Division's LBT narrowed to RM0.2 million (Q3'2024: RM0.8 million).

For the nine months ended 30 September 2025, the Division recorded lower revenue of RM97.0 million (-8.9% YoY) mainly due to lower call-in from OEM customers. Despite recording lower revenue, the Division's LBT narrowed to RM0.1 million (YTD 2024: RM1.3 million) mainly attributable to upward price adjustments and claims received from a customer in 2025.

Marketing Division

For the current quarter ended 30 September 2025, the Marketing Division recorded a 15.3% decrease in revenue (Q3'2025: RM60.7 million; Q3'2024: RM71.7 million) mainly due to softer demand from international OEM customers and weaker sales in Europe, Australia, North America, and Thailand. Despite recording lower revenue, the Division recorded a PBT of RM0.4 million compared to LBT of RM6.9 million in Q3'2024 mainly due to foreign exchange losses resulting from trade receivables denominated in foreign currencies in the same period last year.

For the nine months ended 30 September 2025, the Marketing Division registered a lower revenue of RM194.7 million (-7.6% YoY) mainly due to softer demand from international OEM customers and weaker sales in Europe, Australia, and Thailand. Despite recording lower revenue, the Division recorded a PBT of RM1.0 million compared to LBT of RM4.2 million due to the same reason explained above.

Non-Reportable Segment, Malaysia

This segment comprises mainly operations relating to revenue received from sources that include the rental of properties in Malaysia, provision of management services, and engineering and research services for companies within the Group. Revenue generated from these services and sources form part of the inter-segment elimination for the total Group's results (as depicted in Note A9). This segment also comprises the Group's investment and participation in associate.

For the current quarter ended 30 September 2025, this segment's revenue increased by 2.6% to RM12.7 million from RM12.4 million in Q3'2024 mainly driven by higher inter-group billings for services. In line with the higher revenue and unrealised fair value gains from other investments, this segment recorded a lower LBT of RM1.7 million compared to LBT of RM4.9 million in the corresponding quarter last year.

For the nine months ended 30 September 2025, this segment's revenue increased by 6.7% to RM39.1 million from RM36.7 million in YTD 2024 mainly driven by higher inter-group billings for services. LBT reduced to RM5.4 million from LBT of RM12.0 million in YTD 2024 due to the same reasons explained above. The higher LBT in YTD 2024 was partly attributable to the impairment charge on certain research and development expenditures.

Indonesia Operations

Indonesia Operations refer to the manufacturing and supply of suspension products such as coil springs, shock absorbers and leaf springs as well as the Group's investment and participation in joint ventures and associates in Indonesia.

For the current quarter ended 30 September 2025, the Indonesia Operations recorded revenue of RM18.3 million, down by 17.9% from RM22.3 million in the corresponding quarter last year. The reduction in revenue was primarily due to lower demand from OEM and REM segments. In line with the lower revenue, the Indonesia Operations posted a LBT of RM1.1 million compared to PBT of RM2.1 million in the same quarter last year. The higher PBT in the same quarter last year was boosted by the write-back in provision for doubtful debts following settlement with certain customers and higher share of profit from the Group's joint ventures.

For the nine months ended 30 September 2025, Indonesia Operations recorded lower revenue of RM60.0 million (-7.4% YoY), primarily due to the same factors explained above, partially offset by the commencement of supply to a new OEM customer. In line with the lower revenue, the Indonesia Operations posted a LBT of RM0.2 million compared to PBT of RM2.2 million in the same period last year. The higher PBT in the same period last year was boosted by the same reasons explained above.

All Other Segments

This business segment refers to the Group's operations in Vietnam, Australia, USA, the Netherlands, Thailand, Myanmar and the United Kingdom ("Operations Outside Malaysia").

For the current quarter ended 30 September 2025, Operations Outside Malaysia recorded revenue of RM41.2 million, an increase of 1.5% from RM40.6 million recorded in the same quarter last year. The improvement was primarily attributable to the higher REM demand in USA operations coupled with the improved market conditions for bus and train seats in Australia operations, partially offset by the end of production for an OEM model in Vietnam operations. In line with the higher revenue, this segment recorded a PBT of RM0.9 million compared to LBT of RM2.6 million in the corresponding quarter last year.

For the nine months ended 30 September 2025, this segment recorded a decrease in revenue to RM119.2 million (-0.9% YoY), while LBT narrowed to RM1.4 million compared to LBT of RM8.9 million in the corresponding period last year due to the same reasons explained above. The higher LBT in YTD 2024 had also been adversely impacted by the impairment charge on certain machineries as well as the provisions made for slow moving inventories in certain operations.

Commentary On Prospects and Targets, Strategies and Risk

APM is principally involved in the design, manufacturing, assembly and production of automotive and mobility components. The Group's main operations are located in Malaysia, but it is also present in various other jurisdictions, including USA, the Netherlands, Australia, Thailand, Vietnam, the Republic of Indonesia and the United Kingdom.

Following a record year for the Malaysia's automotive industry in 2024, both in terms of sales and production - the Total Industry Volume (TIV) and Total Industry Production (TIP) declined in the first nine months of 2025, as anticipated. TIV for YTD 2025 contracted by 3% to 579,336 units from 595,883 units in YTD 2024, while TIP fell 7% to 552,129 units from 593,045 units in YTD 2024. Looking ahead, the Group expects both TIV and TIP to remain below 2024 levels for the remainder of 2025, due to shrinking order backlogs and the rising share of electric vehicle sales, which are largely imported as Completely Built-Up (CBU) units. Nevertheless, the Group remains optimistic on Malaysia's automotive industry achieving TIV forecast of 780,000 units set by The Malaysian Automotive Association ("MAA") for year 2025, driven by non-extension of tax exemption for CBU electric vehicle, introduction of new car models, as well as ongoing year-end promotional campaigns offered by carmakers.

The export segment continues to face headwinds arising from tariff uncertainties and ongoing trade-related challenges in key markets. In addition, the impact of currency movements (i.e. Ringgit strengthening) continued to weigh on profitability and competitiveness. The Group also expects continued competitive pressure from new entry of imported products in the domestic REM segment.

Overseas operations remain affected by tariff-related uncertainties and prolonged trade tensions. In Indonesia, the automotive sector is experiencing soft vehicle sales amid a subdued domestic economy and the absence of fiscal stimulus. Despite these conditions, the Group remains cautiously optimistic, underpinned by its diversified customer base and extensive product portfolio. Additionally, the Group sees potential upside from the entry of new Chinese automotive brands into regional markets, which could open opportunities for component supply partnerships and localisation initiatives.

The Group remains vigilant amid ongoing global economic challenges. While geopolitical tensions continue to pose potential risks to financial markets and economic activity, the Group is taking a measured and proactive approach to safeguard its operations.

Looking ahead, the Group is focused on executing its five-year strategic plan, designed to drive long-term business resilience, capitalize on growth opportunities, and consistently deliver sustainable value to its shareholders.